Strategic Wealth Partners was acquired by Kovitz Investment Group Partners, LLC ("Kovitz"), a registered investment adviser with the SEC on May 1, 2024. Strategic Wealth Partners is now a division of Kovitz and its registered investment adviser. Materials created prior to this date were created by Strategic Wealth Partners and are accurate as of the time of publishing.

Seeking Risk v. Managing Risk – I Have a Long Time to Invest, But Am I Putting My Savings Plans at Risk?

January 13, 2021

As savers and investors, there are several elements we can control and many others we cannot. Certainly market returns cannot be controlled, although their results matter a great deal. On the other hand, we can control our ability to save and how much portfolio risk we take; these are two areas that are very impactful in determining the long-term likelihood of a successful financial plan.

The focus of this article will be on integrating two previous SWP blog topics:

The impact of sequence risk (aka sequence of return risk) on portfolio outcomes was the topic of the article The Risk You May Not Have Considered, co-authored by David Copeland and Cory Rappaport.

In the sections ahead, we’ll profile two individuals confronted by different but similar issues pertaining to saving and investing.

Let’s begin by visiting with Blake and Taylor. Here is some background:

Both are in their early thirties.

Each has the same initial time horizon of 21 years for saving and investing. At the end of this period, they will re-evaluate their pre- and post-retirement plans.

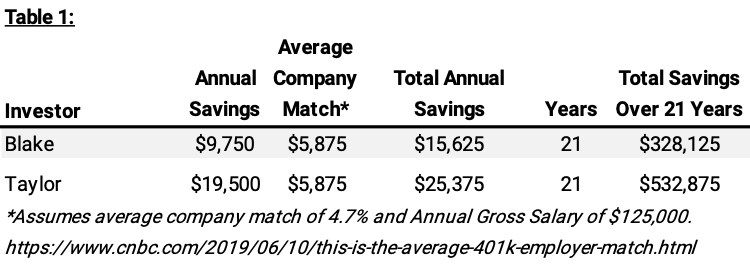

Both individuals earn the same annual gross salary of $125,000 and work for companies that provide a 401(k) retirement plan match.

Blake spends more than Taylor, so Taylor can save more in the 401(k) plan.

Table 1 below provides an overview of their respective savings, including projected totals over 21 years (note that Table 1 shows savings only; earnings are considered in the following section).

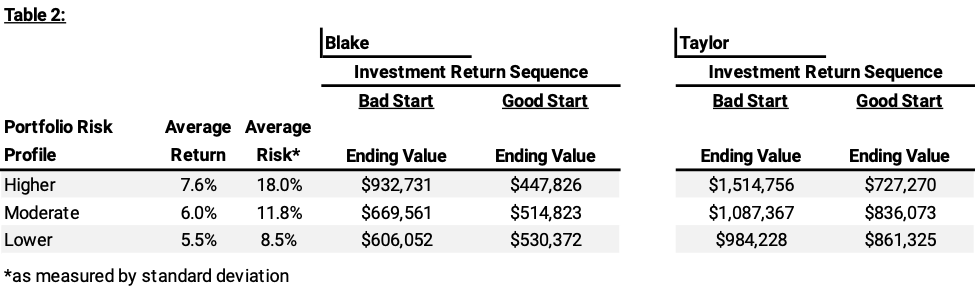

With a review of their savings plans complete, Blake and Taylor turn their focus to investing their hard-earned money. Given their age and time horizon, they feel they are willing and able to take more risk by investing aggressively in stocks within their respective 401(k) accounts. They’ve talked to some of their friends, and many have advised them to “just buy stock funds.” However, they remembered a recent 401(k) information session that highlighted the importance of diversification and managing risk. With access to an advisor through their 401(k) provider, they scheduled a meeting to review how risk and return may influence their long-term savings plans.

Table 2 below shows the output of three different hypothetical portfolios:

Higher risk profile – Invested exclusively in a U.S. large-cap stock fund.

Moderate risk profile – Invested 50%-70% in stock funds with the remainder in bond funds.

Lower risk profile – Invested 30%-50% in stock funds with the remainder in bond funds.

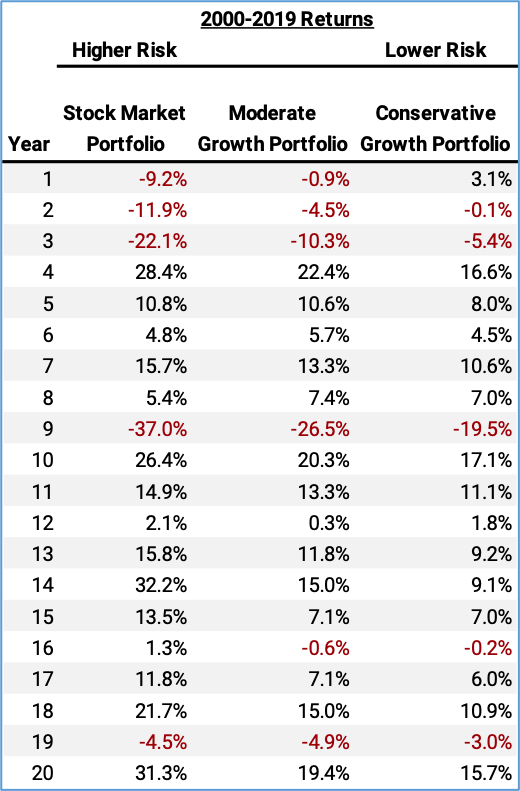

Table 2 below includes two investment returns sequences: “Bad Start” and “Good Start.” The investment return sequence titled “Bad Start” is the actual return outcomes from 2000 to 2019, while the sequence titled “Good Start” is the same annual returns but in reverse order. During the early 2000’s the market performed very poorly, while in the last several years of that period, equity markets performed very well and generated above average historical returns.

The advisor explains that in the early years, losses on the smaller investment balance are far less impactful in dollar terms than the losses occurring later, on the much larger investment balance. She follows with, “losses are actually welcomed during the early period because it allows a saver to invest more at lower prices!”

Blake says, “So, it’s sort of like buying an investment when it is on sale?”

The advisor responds enthusiastically, “YES! Exactly…but unlike many online sale purchases, this one doesn’t follow with a load of junk e-mail after your purchase!”

The advisor then highlighted that this is the opposite of what happens in retirement when investors draw on their portfolios for income needs; when portfolio returns are worse to start, the withdrawals could have a distressing effect on the portfolio value versus if portfolio returns are better to start. That’s because there’s a compounding effect of withdrawing funds from a declining balance – exactly the opposite of buying during a sale.

After reviewing the analysis and talking with the advisor, Blake and Taylor recognize an opportunity to do more ‘fine-tuning’ for their own respective portfolios before deciding on the best path forward. It is clear to each of them now how risk can work against them and their well-intentioned savings plans.

Blake and Taylor’s story is not intended to suggest, or recommend, what the right level of savings or portfolio risk is; we understand everyone has different goals, objectives, and preferences. Rather, our goal is to highlight several key elements of the wealth-building process that play an important role in determining the likelihood of long-term success.

As illustrated in our story, saving and risk exposure have a meaningful impact on long-term outcomes. Notably, it may be the case that a relatively better savings plan allows an investor to assume considerably less risk without compromising the ability to meet their goals. Therefore, the elements Blake and Taylor can control end up creating real outcomes that matter later in life.

If you’re reaching a period in your career where you’re accumulating higher levels of savings, please reach out to your SWP advisor to review how these concepts may apply to you. We are always here to help.

There’s nothing easy about divorce. It can feel as though your entire life changes overnight, and for ultra-high-net-worth (UHNW) individuals, the financial implications can be just as overwhelming as the emotional ones. One of the most overlooked yet critical aspects of this transition is estate planning.

I recently worked with a client, we’ll call her Laura, who had just finalized a divorce after 27 years of marriage. She had always been involved in the family’s finances, but for the first time, she was solely responsible for her own estate. Her first question to me was, “Where do I even begin?”

If we’ve worked together for any length of time, you know I regularly talk and write about investor psychology, especially how tuning out day-to-day market headlines can lead to better long-term results. In a world full of distractions, this mindset is more important than ever.

We live in an era of nonstop financial news. From interest rate speculation and economic forecasts to geopolitical tensions and trade policy shifts, headlines are constantly vying for our attention and our reaction.

Recently, headlines about new tariffs and another downgrade of U.S. government debt have added fresh layers of uncertainty. And naturally, these stories raise questions:

Should I adjust my portfolio? Go to cash? Do something, anything, right now?

Our team regularly reads articles from industry peers and trusted resources to stay up to date on financial markets. We enjoy reading about topics related to economics, investments, current events, and financial planning.

In addition to circulating some of the best pieces internally, we thought our clients, partners, and friends might enjoy reading some of the same articles as us.

Here are recent pieces that our team members have read, along with some commentary on why we found the respective articles interesting.